Most investors can explain what a bond is in one sentence. They can usually describe a dividend stock, a REIT, or even a commodity ETF without much trouble. Mineral interests are different. Even though they are tied to real property, real production, and real cash flow, they are still one of the most misunderstood asset classes in America.

That confusion does not exist because mineral interests are unimportant. It exists because they sit at the intersection of real estate, energy, private markets, and legal title, yet they do not behave exactly like any of those categories. For decades, that made them hard to access, hard to compare, and easy to mislabel.

At Mineral Vault, we believe this confusion has caused many investors to overlook an asset class that deserves a much closer look. Once mineral interests are understood on their own terms, the picture becomes much clearer: they are not direct drilling deals, they are not fixed income, and they are not just another form of public-market energy exposure. They are a distinct form of real-asset ownership with a return profile that many investors have rarely had a fair chance to evaluate.

Why the confusion starts so early

Most people first hear about oil and gas investing through the wrong lens. They think about drilling risk, wildcat wells, giant capital budgets, or public energy stocks that rise and fall with commodity headlines. Mineral interests are often grouped into that same mental bucket, even though the economics can be very different.

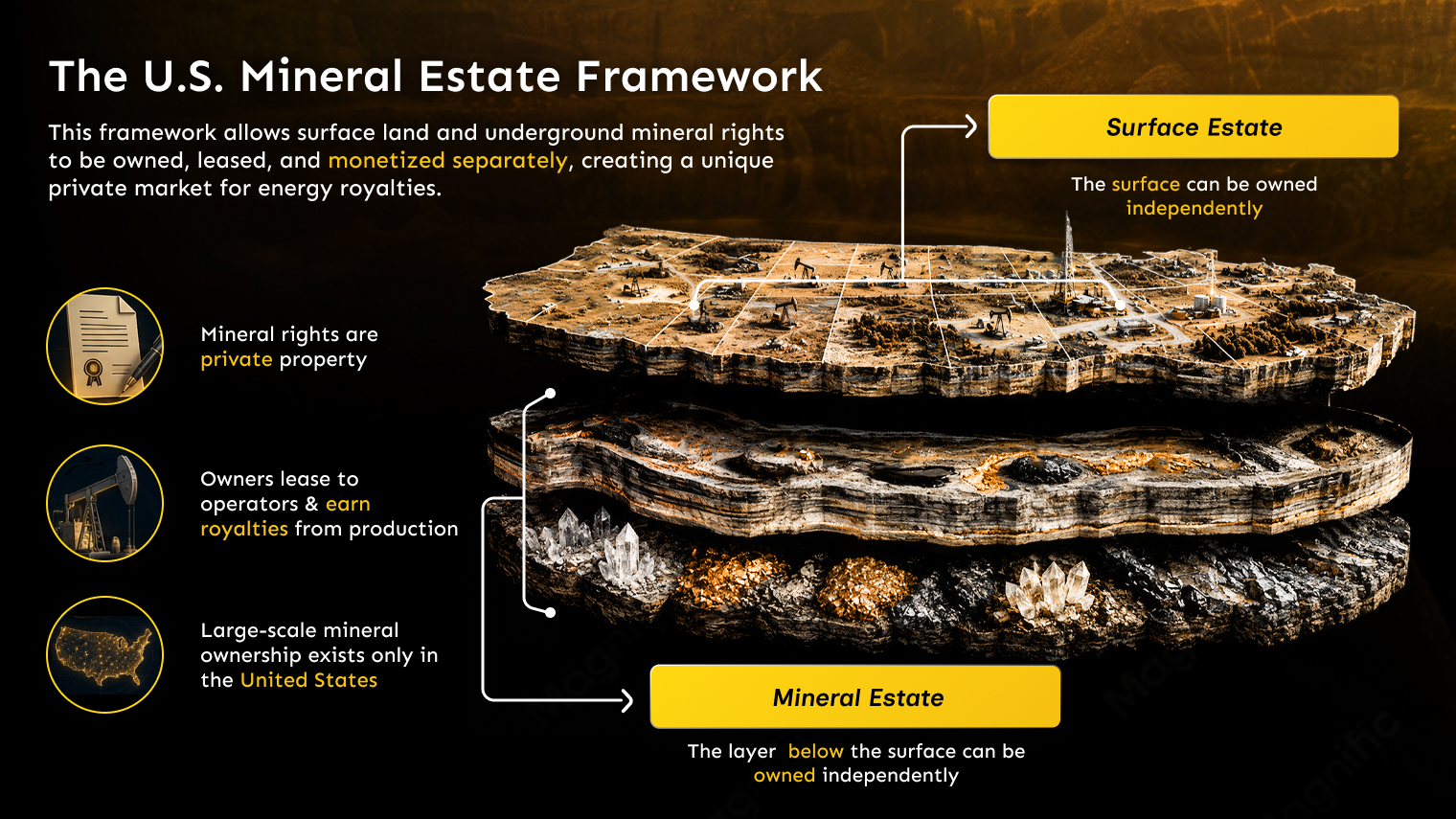

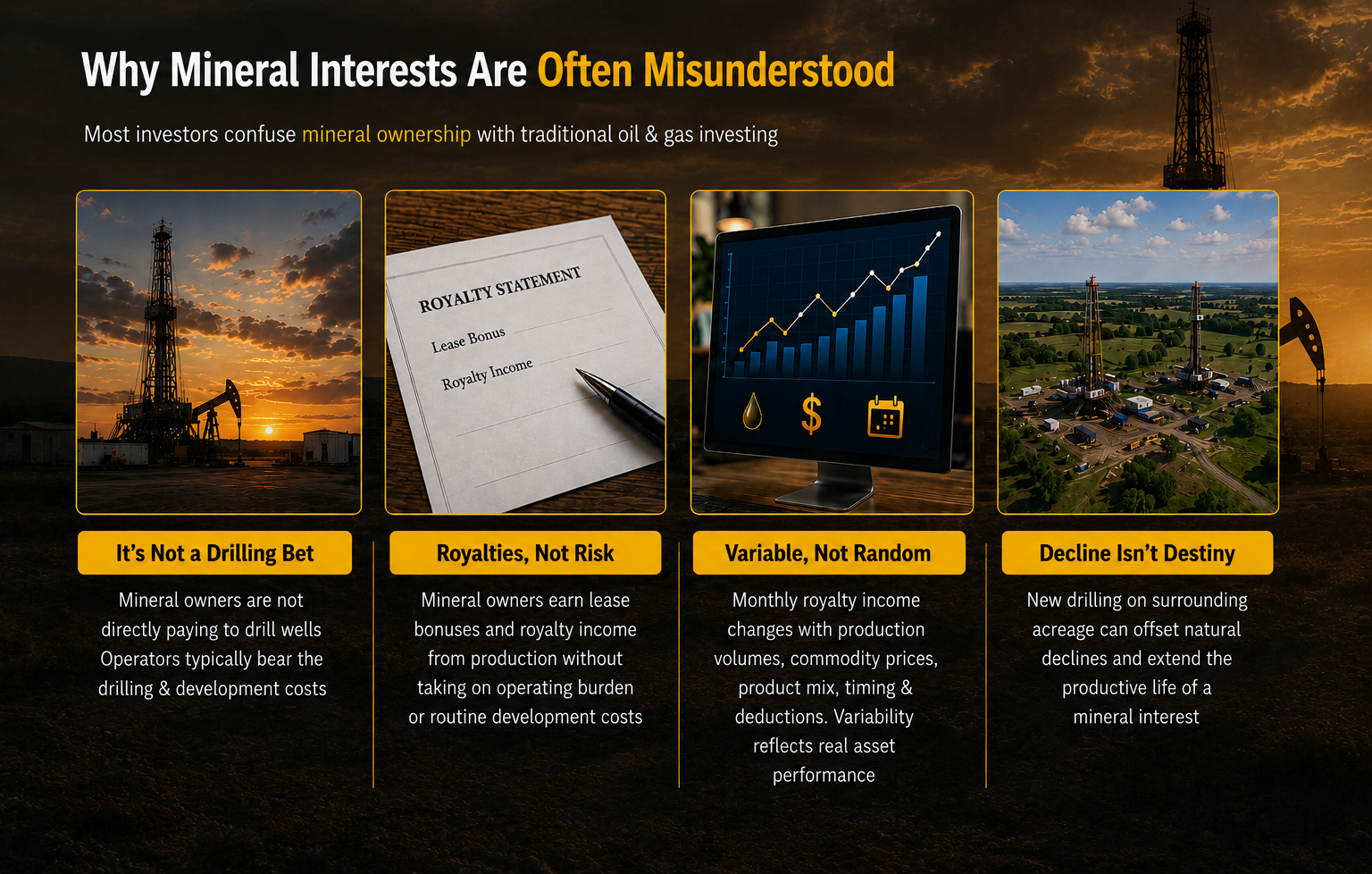

A mineral interest is a real property right. When the underlying acreage is leased and production occurs, the mineral owner can receive lease bonuses and royalty income from the operator’s extraction activity. That is a very different position from being the company paying to drill the well. In many cases, the mineral owner benefits from production without taking on the same operating burden or routine development costs that come with a working interest.

That distinction matters, but it is easy to miss. The words used in the industry — minerals, royalties, overriding royalties, working interests, net revenue interests, term assignments, division orders — are not intuitive to most investors. When the vocabulary is unfamiliar, the whole asset class can look more exotic and opaque than it really is.

Mineral interests are real property, but they do not look like traditional real estate

Another reason mineral interests are so misunderstood is that they are a form of real estate that most people never physically see. A house, warehouse, apartment building, or office property is easy to visualize. Mineral interests are different because the economic value sits below the surface.

That can make them feel abstract, even though the legal foundation is concrete. Mineral interests are ownership rights in the subsurface estate. Their value comes from the natural resources that may be extracted from that acreage, and their cash flow comes from production and lease activity rather than from rent checks or tenant demand.

This is one reason mineral interests are often misclassified. They share some traits with real estate, but they do not behave like plain commercial property. They share some traits with commodity exposure, but they are not simply a bet on spot prices. They can generate income, but they are not a bond. Investors looking for a familiar legacy bucket often end up forcing mineral interests into the wrong one.

Many investors confuse mineral interests with direct drilling exposure

This is probably the biggest misunderstanding of all. When people hear “oil and gas,” they often assume the investment must be cost-heavy, operationally messy, and exposed to the full burden of drilling and development. That assumption can be true for certain energy investments, but it is not the default reality for mineral and royalty ownership.

Mineral Vault’s public materials make this distinction clear. In general, the mineral and royalty interests associated with its offerings are not cost-bearing in the same way working interests are. The operator usually bears the majority of drilling and development costs, while the owner of the mineral interest receives lease bonuses and royalty payments tied to production. That does not mean the investment is cost-free in every possible sense — property taxes, withholding tax effects, management fees, and minor entity-level costs still matter — but it does mean the economics are often very different from what many investors imagine when they think about oilfield risk.

When mineral interests are incorrectly treated as if they were direct participation in drilling programs, investors can overestimate some risks while completely missing other characteristics that actually define the asset class: passive exposure, real-asset linkage, portfolio diversification, and cash flow that comes from production rather than from operating a business.

The cash flow is variable, but it is not arbitrary

Mineral interests are also misunderstood because their income does not behave like a fixed coupon. Some investors see variable monthly distributions and assume the asset is unreliable. In reality, the variability is usually the natural result of how the underlying properties work.

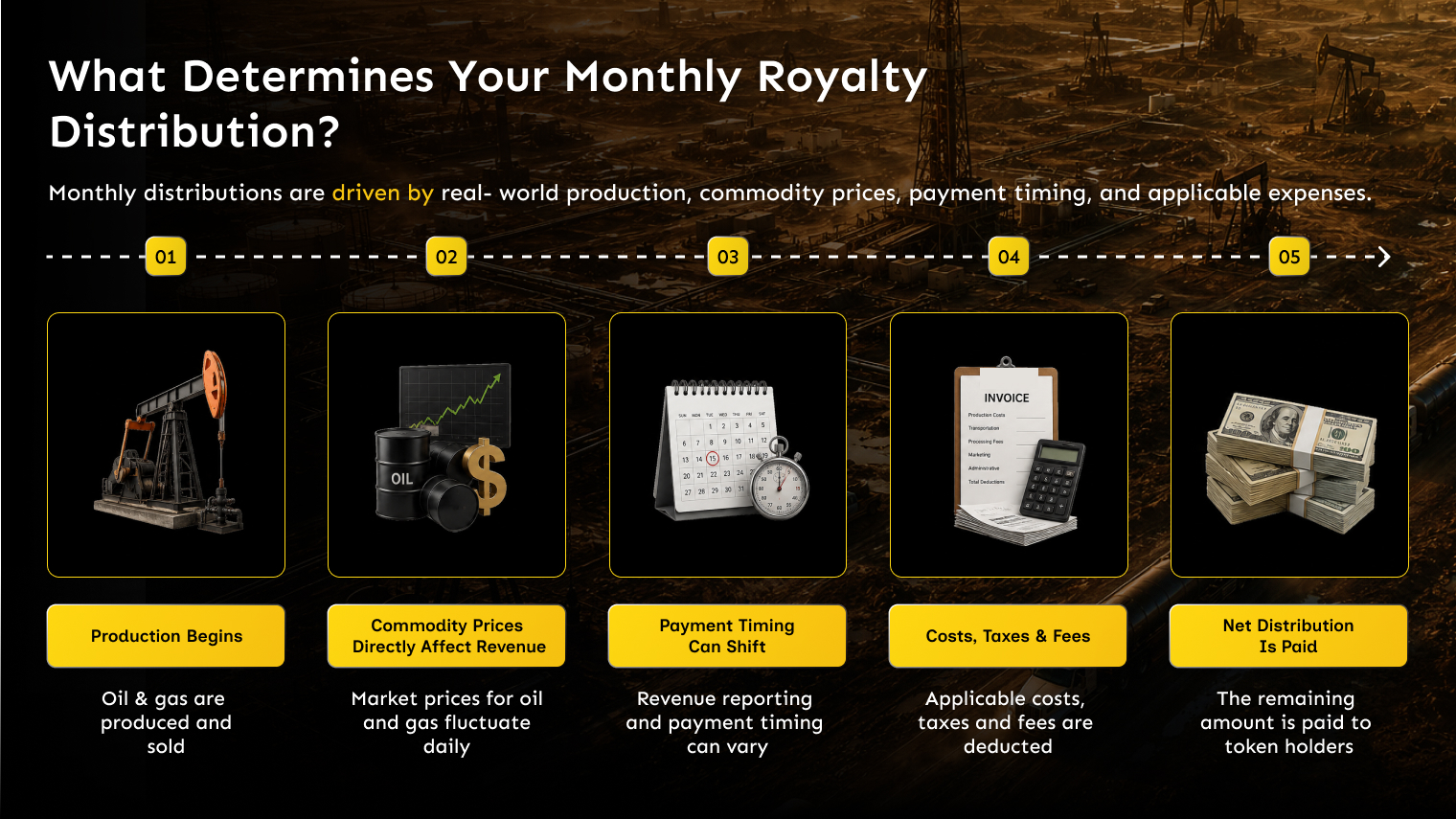

Royalty income can move from month to month because of production volumes, oil and gas prices, product mix, maintenance, downtime, timing differences in operator reporting, and changes in deductions such as property taxes or withholding. That variability is real, but it is not random. It reflects the performance of real producing assets.

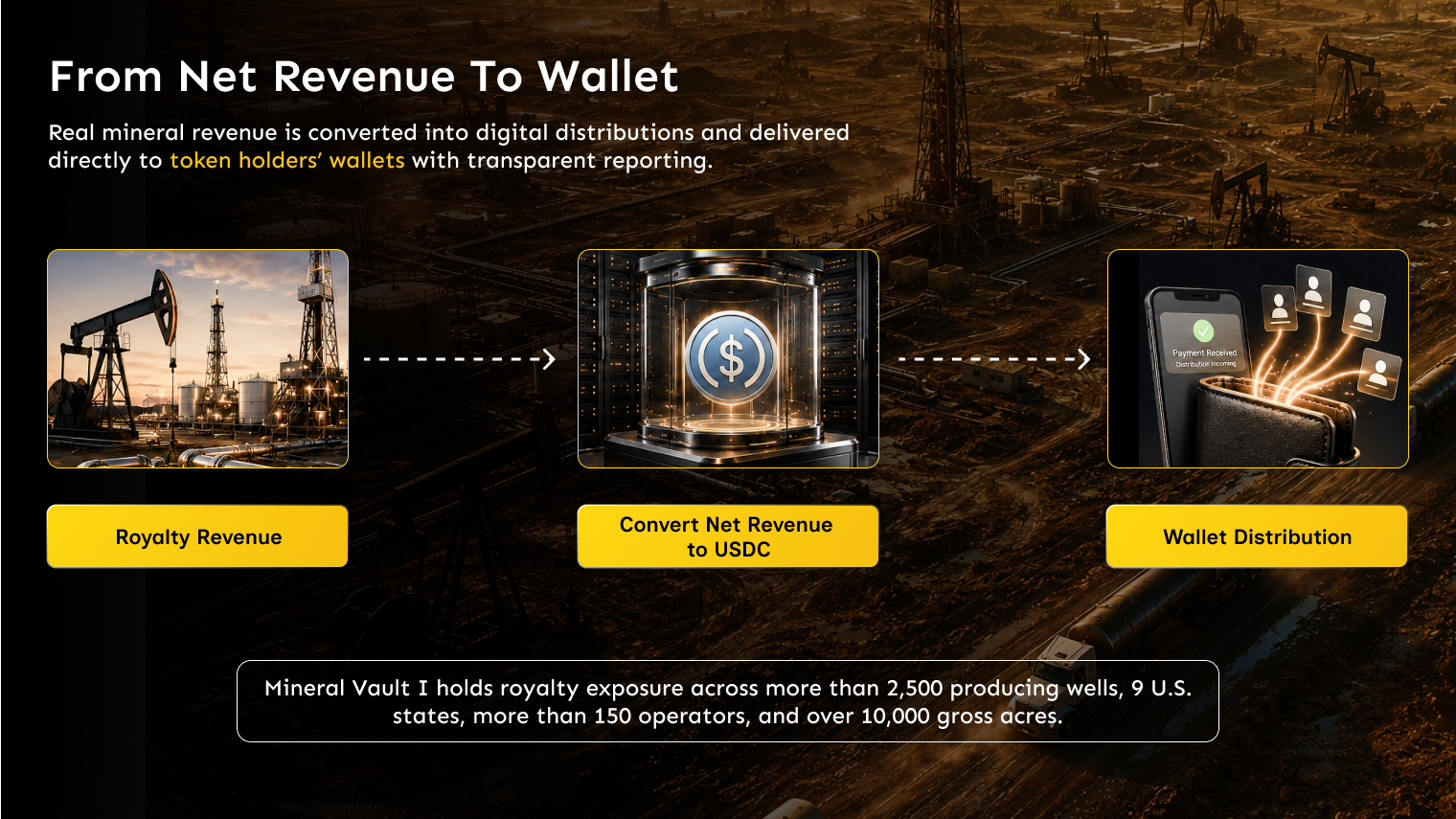

Mineral Vault’s structure is designed to make those mechanics easier to follow. Revenue flows from the source entity to the tokenized SPV, monthly distributions are made to token holders, and supporting documentation is published through the transparency page, including dividend reports, spreadsheets, and underlying support for line items. That kind of reporting helps investors understand what changed and why, rather than simply seeing a payout number with no context.

In other words, the misunderstanding is not just about the asset itself. It is also about visibility. When investors cannot easily see what is driving a distribution, they may assume the cash flow is unpredictable by nature. Better reporting does not remove variability, but it does make the cash-flow logic much more intelligible.

Depletion is real, but that is not the whole story

Another reason mineral interests are misunderstood is that the conversation usually stops at depletion. People hear that oil and gas wells decline over time and conclude that the whole category must simply be a shrinking stream of income. Depletion is absolutely real, and investors should understand that clearly. Mineral Vault itself says production volumes and cash flows are likely to decline over the 15-year term of a tokenized offering as depletion takes place.

But that is not the whole story, especially in a large, diversified portfolio. Mineral Vault also emphasizes future drilling potential and acknowledges that operators may drill new wells on tokenized properties, creating new production streams that can offset some of the decline from older wells. This is the reserve replacement dynamic.

That matters because a diversified portfolio does not behave like a single-well bet. Some wells are older. Some are newer. Some operators are more active than others. Some acreage is already productive, while some surrounding acreage may still support additional development later on. When reserve replacement occurs across a portfolio of this scale, the overall decline profile can be softer than what an investor might expect if they are thinking only in terms of one well depleting in isolation.

Reserve replacement does not eliminate depletion, and it should never be described that way. What it can do is make the aggregate portfolio behave differently from the simple mental model many people bring to the category. That nuance is one of the most important things modern investors need to understand about mineral interests.

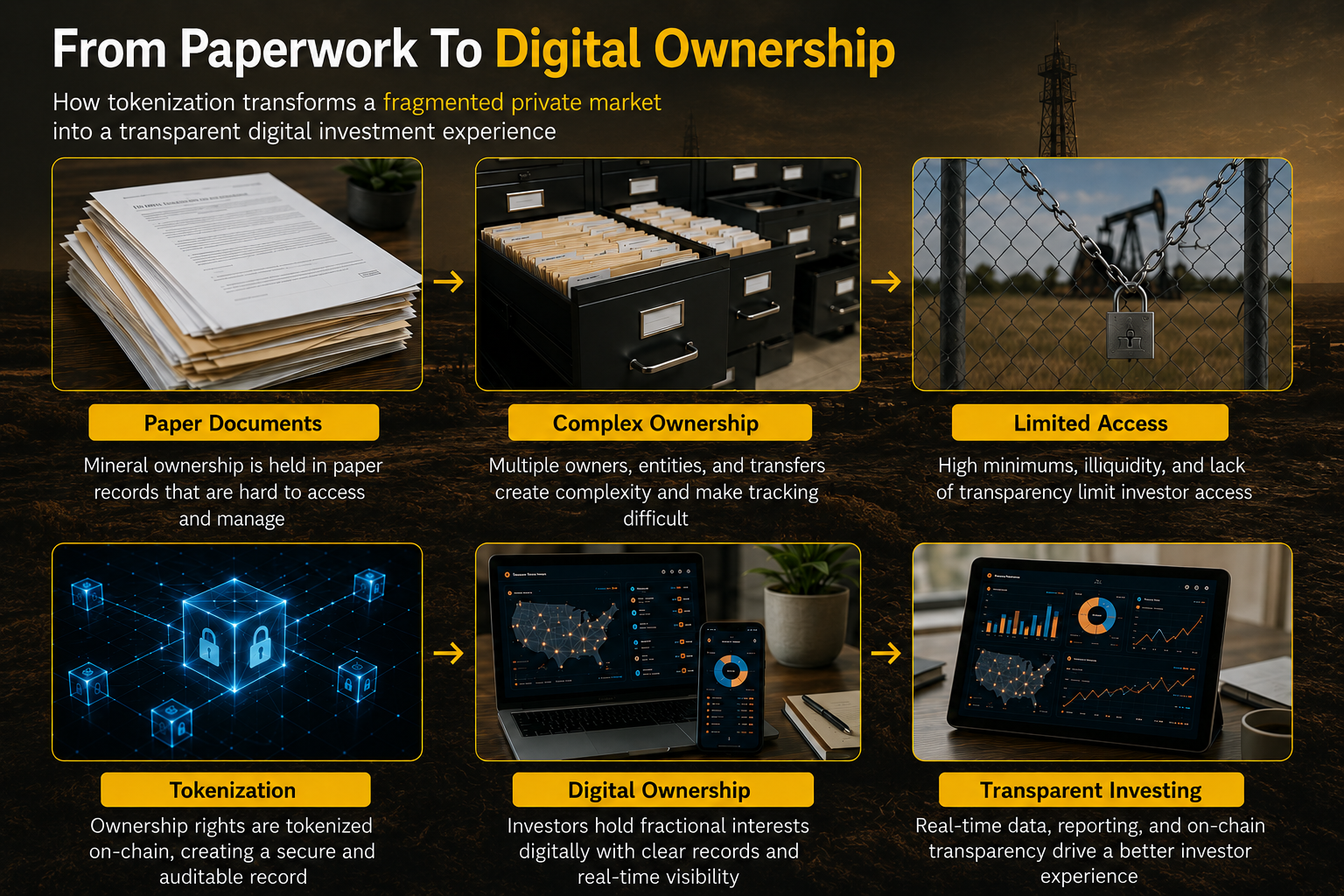

The asset class has historically been buried under paperwork and private-market friction

A big part of the misunderstanding is not conceptual at all. It is operational. For decades, mineral interests have been difficult to buy, difficult to diligence, difficult to transfer, and difficult to monitor. That has kept the asset class mostly inside specialist circles.

Traditional ownership often involves fragmented documentation, title complexity, private negotiations, paper-heavy transfer processes, and large capital commitments. Even when the economics are attractive, the ownership experience has rarely felt modern. That creates a strange problem: a real asset with real value ends up looking obscure simply because the infrastructure around it has been outdated and inaccessible.

Mineral Vault was built to change that experience. Its platform uses a tokenized SPV structure to package financial exposure to a diversified set of U.S. mineral and royalty interests into a format designed to be easier to own, easier to transfer, and easier to track. Monthly digital distributions, on-chain ownership records, and public transparency materials do not change the underlying geology, but they do change how investors can engage with the asset class.

Why mineral interests deserve a more accurate place in portfolio conversations

Because the category is so often misunderstood, it is often left out of modern portfolio discussions altogether. Investors usually default to familiar income buckets: bonds for contractual cash flow, dividend stocks for corporate payout growth, and REITs for listed real-estate exposure. Mineral interests do not fit neatly into any one of those categories.

They are best understood as a distinct real-asset income allocation. They can provide exposure to U.S. energy production cash flows, inflation-linked revenue dynamics, and upside from future development, all without requiring the investor to operate wells or fund large drilling budgets directly. At the same time, they come with their own tradeoffs: commodity sensitivity, legal and tax complexity, depletion over time, and a return profile that does not map perfectly onto legacy public-market products.

That is exactly why a better framework matters. If investors mistake mineral interests for bonds, they will misunderstand the variable nature of the cash flow. If they mistake them for direct drilling programs, they will misunderstand the cost structure. If they mistake them for plain real estate, they will misunderstand the revenue drivers. And if they treat them as just another energy stock proxy, they will miss the property-rights foundation that makes them different in the first place.

Where Mineral Vault changes the picture

Mineral Vault’s role is not to pretend this asset class is simple just because it is now tokenized. The point is to make a historically difficult asset class more legible, more accessible, and more transparent.

The platform’s current public materials describe Mineral Vault I as a tokenized vehicle backed by cash-flowing U.S. mineral properties, with monthly USDC distributions, published dividend support, and a structure in which revenue flows into an SPV and then out to token holders after applicable expenses. The properties are selected for current cash flow, future drilling potential, and diversification across location, operator, well type, and resources produced.

That matters because one of the best ways to reduce misunderstanding is to let investors see the asset class more clearly. Better structure, better reporting, and better access do not remove every risk. They do, however, remove some of the old barriers that made mineral interests feel invisible or reserved only for insiders.

Key takeaways

- Mineral interests are often misunderstood because they sit between multiple familiar asset categories without fitting perfectly into any of them.

- They are real property rights, not just generic commodity exposure and not the same thing as direct drilling participation.

- Their cash flow is variable because it is tied to real production and real market conditions, not because it is arbitrary.

- Depletion matters, but in diversified portfolios, reserve replacement and future drilling potential can materially change how the overall asset behaves over time.

- Historically, private-market friction and paper-heavy ownership structures helped keep the asset class obscure.

- Tokenization, transparency, and digital distributions can make mineral interests easier to understand, monitor, and evaluate in a modern portfolio context.

Final thought

Mineral interests are not misunderstood because they are weak. They are misunderstood because they have spent too long living outside the frameworks most investors use every day. They do not trade like common stocks, they do not pay like bonds, and they do not look like surface real estate. That difference has often been treated as a reason to ignore them. We think it is a reason to understand them better.

For investors seeking real-asset exposure, passive income tied to productive U.S. properties, and a return profile that does not simply mimic the usual public-market categories, mineral interests deserve much more serious attention than they typically receive.

Disclaimer: This article is educational in nature and should not be considered investment, tax, or legal advice.