A common mistake in income investing is to assume that every monthly payout should behave like a fixed coupon. That is not how mineral royalties work. A royalty distribution is not manufactured in a spreadsheet and pushed outward on a schedule regardless of market conditions. It begins with real oil and natural gas production, real purchaser payments, and real operating activity across the underlying property portfolio.

That is exactly why mineral royalty income can be so compelling. The cash flow is tied to producing assets, but the amount distributed in any given month will move with what the assets actually did. Some months are stronger. Some are softer. The important point is that the changes are usually explainable. They are variable, but they are not random.

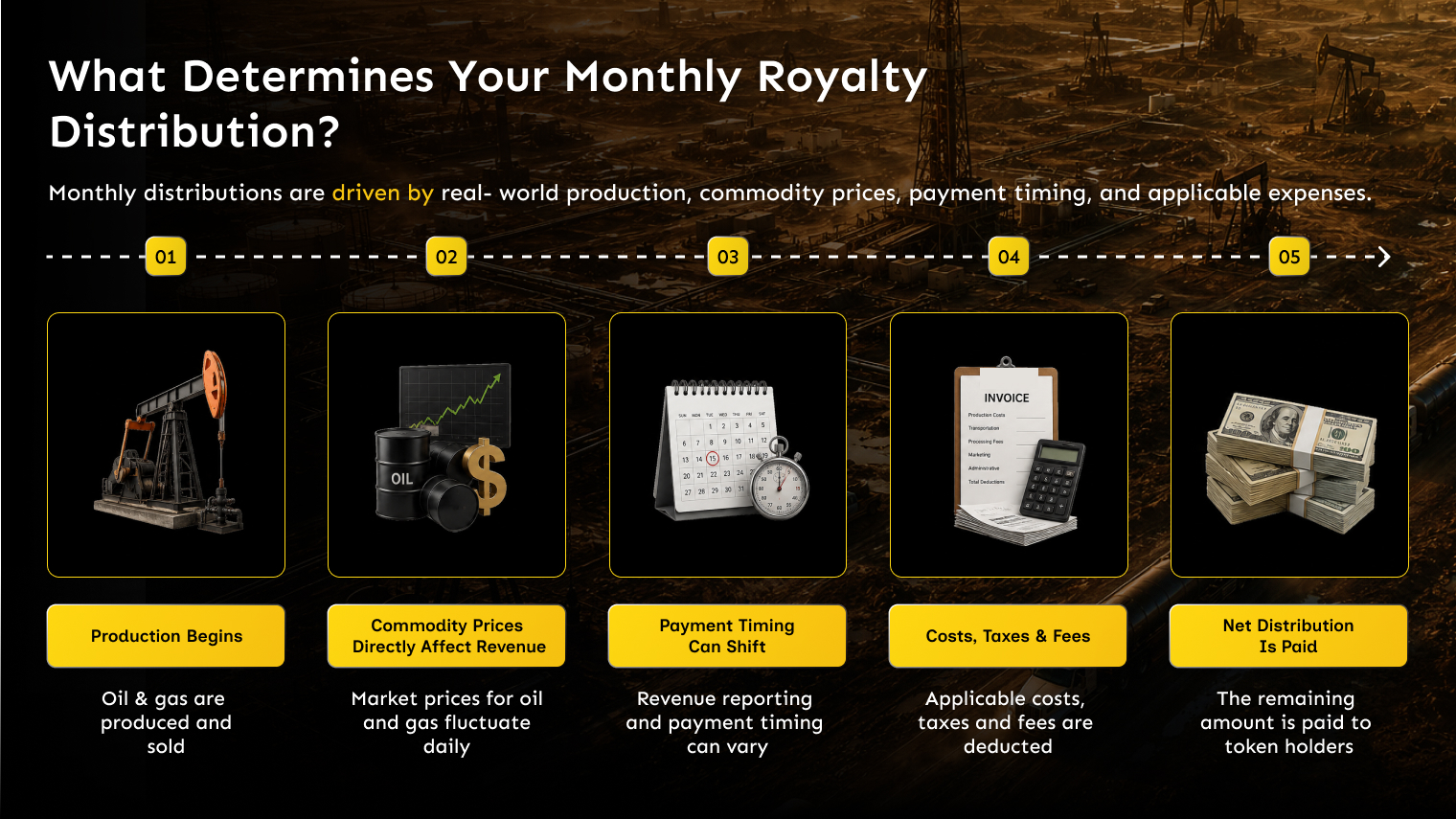

For Mineral Vault I, the right way to think about a monthly royalty distribution is as the end result of a chain: hydrocarbons are produced and sold, revenue is collected, eligible expenses and fees are accounted for, and the remaining distributable amount is paid to token holders in USDC. Once investors understand the moving parts inside that chain, month-to-month changes become much easier to interpret.

It Starts With Production and Sale

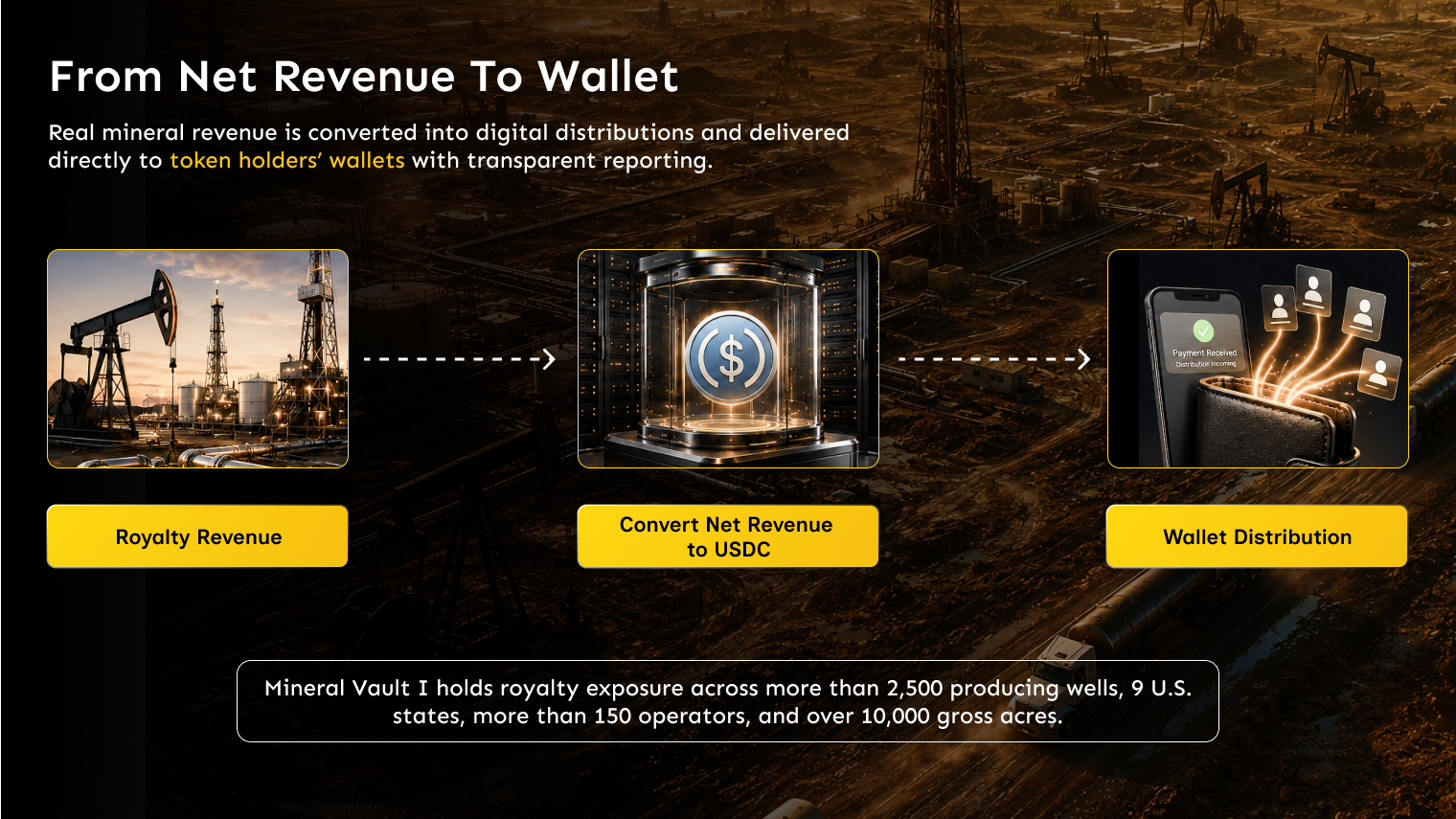

Every royalty distribution begins at the wellhead. Mineral Vault I holds royalty exposure across more than 2,500 producing wells, 9 U.S. states, more than 150 operators, and over 10,000 gross acres. Those wells generate revenue only when crude oil, natural gas, and natural gas liquids are actually produced and sold. No production means no revenue. Higher production generally means more revenue. Lower production generally means less.

That sounds simple, but the implications matter. A royalty distribution is fundamentally different from a bond coupon because it is tied to operating assets. Wells do not produce the exact same amount every month. Some decline naturally. Some are temporarily offline for maintenance. Some are constrained by weather, takeaway capacity, or routine field work. Some may outperform expectations. In a large portfolio, all of those moving pieces are happening at once.

This is why one month should never be viewed in isolation. A single distribution is only a snapshot of how the portfolio performed during that collection period. The better question is always: what changed in the underlying production base?

Commodity Prices Directly Affect Gross Revenue

Production volumes are only half of the equation. The same barrels and the same gas volumes can generate materially different revenue from one month to the next if commodity prices move. Mineral Vault’s assets are sold at or near commodity spot prices at month-end, which means realized revenue naturally reflects the pricing environment rather than a fixed contract-like payment stream.

When oil prices rise, royalty revenue can rise even if production is relatively stable. When natural gas prices weaken, revenue can fall even if wells are still producing. Product mix matters as well. A portfolio that receives revenue from crude oil, natural gas, natural gas liquids, and occasional lease bonuses will not move in exactly the same way every month because those revenue streams do not always move together.

That variability is not a flaw in the model. It is part of what gives mineral interests their real-asset character. The distributions are connected to actual energy production and market pricing rather than to a fixed promise detached from the assets themselves.

Timing Matters More Than Many Investors Expect

Even when commodity prices and production are understood correctly, the month in which cash is actually received can still shift. Operators and purchasers do not always remit proceeds on a perfectly uniform timeline. Statements can arrive on different schedules. Certain wells may have short-term payment timing differences. Adjustments can also be booked after the fact.

That means a monthly distribution can sometimes reflect timing as much as economics. In other words, a softer month does not always mean the asset base itself became weaker. It can simply mean that part of the revenue cycle landed in the following distribution period instead of the current one.

This is one of the reasons transparency matters so much in royalty investing. Without visibility into the revenue and expense trail, investors may misread normal timing noise as a fundamental change. With clear reporting, the difference becomes much easier to understand.

The Net Distribution Is Calculated After Real Costs and Fees

Gross revenue is not the same thing as distributable revenue. Once royalty income is received, the tokenized SPV accounts for the costs that actually apply to the portfolio. Mineral Vault has been very clear that these costs are payable from revenue received by the SPV itself, not through future capital calls to token holders.

The largest recurring items include property taxes, minor expenses on revenue, and management fees. Property taxes on producing U.S. oil and gas properties are a real economic cost of owning the assets. Mineral Vault’s public materials note a rough rule of thumb of around 3% of annual revenue for property taxes, though the actual amount can vary. On top of that, Mineral Vault LLC receives a 10% management fee for ongoing property management, administration, tax and regulatory work, token management, and investor coordination.

In Mineral Vault’s own explanation of the distribution flow, the remaining 90% of net revenue becomes the dividend pool distributed to token holders. That means a month with strong gross receipts can still produce a somewhat different net distribution depending on the exact mix of expenses, taxes, and timing adjustments that landed in that cycle.

U.S. withholding tax is another important consideration. Mineral Vault has disclosed that U.S. source income is initially subject to withholding at the SPV level, with filings and potential recoupment handled as part of the structure. For investors, that means there can be a difference between pre-withholding economics and the amount ultimately available on a net basis.

Portfolio Scale Can Help Smooth the Ride

A single well bet can be extremely binary. If that one well underperforms, goes offline, or declines faster than expected, the investor feels the full impact immediately. A large royalty portfolio behaves differently. With thousands of wells, multiple basins, and more than 150 operators, no single well or operator determines the whole outcome.

This does not eliminate volatility. It changes its character. In a diversified royalty portfolio, some wells are declining while others are stable. Some operators are making payments this month while others are slightly later. Some parts of the portfolio benefit more from oil strength, while others are more sensitive to natural gas pricing. The result is not a flat line, but it can be a more resilient income stream than a concentrated single-asset exposure.

This diversification is one of the most important reasons not to overreact to any single monthly figure. The portfolio should be understood as a living collection of producing assets rather than as one decline curve.

Reserve Replacement Can Become a Material Driver

Aside from the obvious factors of prices, volumes, and timing, reserve replacement becomes increasingly important in a portfolio of this size. Oil and gas wells naturally deplete over time. Mineral Vault has been direct about that reality. Production volumes and cash flow are expected to decline over the 15-year term, which is one of the reasons the offering itself is term-limited.

But depletion is not the whole story. Additional wells may be drilled on existing acreage, new production streams can come online, and presently unleased acreage can generate lease bonuses or later drilling activity. Mineral Vault’s public materials explicitly highlight the future drilling potential on more than 10,000 gross acres as a source of both expected and unexpected additional cash flow.

In a portfolio this large, that matters. A single well declines on its own schedule. A large portfolio has the potential for a more dynamic profile because older wells can be partially offset by new wells entering the asset base over time. Reserve replacement does not eliminate depletion, and it should not be described that way. What it can do is lessen the overall depletion rate of the portfolio by continually adding new productive life into the system as fresh wells come online.

That is one of the most important differences between a one-well investment and a broadly diversified royalty portfolio. The latter is still a depleting real asset, but the aggregate decline profile can be materially softer than the decline profile of any single underlying well.

From Net Revenue to Wallet

After revenue is collected and the applicable deductions are accounted for, Mineral Vault converts the distributable amount into USDC and pays it directly to token holders’ wallets. The mechanics of that step are modern, but the economics underneath are still anchored to real mineral interests, real operator payments, and real portfolio performance.

That is an important distinction. Tokenization does not remove commodity price exposure. It does not stop wells from depleting. It does not create artificial yield. What it does is make ownership easier to access, payout delivery more efficient, and reporting substantially more transparent than what investors have historically seen in private energy investing.

Why Transparency Matters When Distributions Move

A variable distribution model only works for investors if they can understand what is driving the variation. That is where Mineral Vault’s transparency framework matters. Dividend reports, supporting documentation, revenue support, expense support, and public-facing summaries all help connect the final distribution amount back to the underlying economics of the portfolio.

In traditional royalty investing, investors often had to wait for paper checks, mailed statements, delayed tax forms, and fragmented reporting. Mineral Vault’s model is stronger because it pairs real producing mineral interests with direct-to-wallet distributions and a much clearer reporting trail. That does not make every month identical. It makes every month more understandable.

The Right Way to Read a Monthly Distribution

The best way to evaluate a royalty distribution is not to ask whether it stayed flat. It is to ask what happened across the portfolio. Were commodity prices stronger or weaker? Were production volumes up or down? Did payment timing shift? Were there any one-time bonuses, taxes, or deductions? Were new wells helping offset legacy decline?

For Mineral Vault I, monthly distributions are the output of a real asset system, not a fixed-income abstraction. That is exactly what makes them interesting. Investors are receiving cash flow tied to U.S. energy production, while benefiting from diversification, tokenized access, direct-to-wallet distributions, and unusually robust transparency. Month-to-month variability is part of that reality. The goal is not to eliminate it. The goal is to understand it.

Why Private Mineral Ownership Is So Rare Globally – And Why That Matters

Why Private Mineral Ownership Is So Rare Globally – And Why That Matters  Mineral Royalties vs. REITs, Dividend Stocks, and Bonds: Where Do They Fit in a Modern Portfolio?

Mineral Royalties vs. REITs, Dividend Stocks, and Bonds: Where Do They Fit in a Modern Portfolio?  Why a Diversified Royalty Portfolio Behaves Differently From a Single Well Bet

Why a Diversified Royalty Portfolio Behaves Differently From a Single Well Bet