When most people think about oil, gas, and other valuable underground resources, they picture governments, national oil companies, and state-controlled licensing regimes. In most of the world, that is the correct mental model. The subsurface belongs to the state, and private parties participate only through concessions, leases, joint ventures, or service contracts granted by the government.

That is precisely why the United States remains so unusual. Here, mineral rights can be privately owned, sold, inherited, severed from the surface estate, and leased to operators in exchange for royalties. That legal structure created an investable market that is rare on a global scale: a market where private owners can hold long-duration rights to underground resources and receive income when those resources are developed.

For Mineral Vault, that is not just an interesting legal footnote. It is the foundation of our asset class. Private mineral ownership is what makes American oil and gas royalties both so compelling and so historically difficult to access. And once investors understand why this ownership model is rare, they also understand why bringing it on-chain matters.

The global rule: governments control the subsurface

Across much of the world, subsurface resources are treated as sovereign assets. Even when surface land is privately owned, the oil, gas, or mineral estate below it is often reserved to the national or regional government. Companies can still explore and produce, but they do so through state-issued rights, negotiated contracts, and regulatory frameworks that do not create the same large-scale private ownership market seen in parts of the United States.

This matters because it changes the entire ownership chain. In a state-dominant system, investors usually gain exposure through public equities, sovereign-linked ventures, production-sharing agreements, debt instruments, or direct corporate ownership in operating companies. What they generally do not gain is a broad market of privately owned mineral interests that can be aggregated, transferred, leased, and monetized over decades the way U.S. mineral properties can.

That is why private mineral ownership at scale is so rare globally. It is not simply a matter of geology. It is a matter of property law, legal history, and the way different countries chose to allocate economic rights in natural resources.

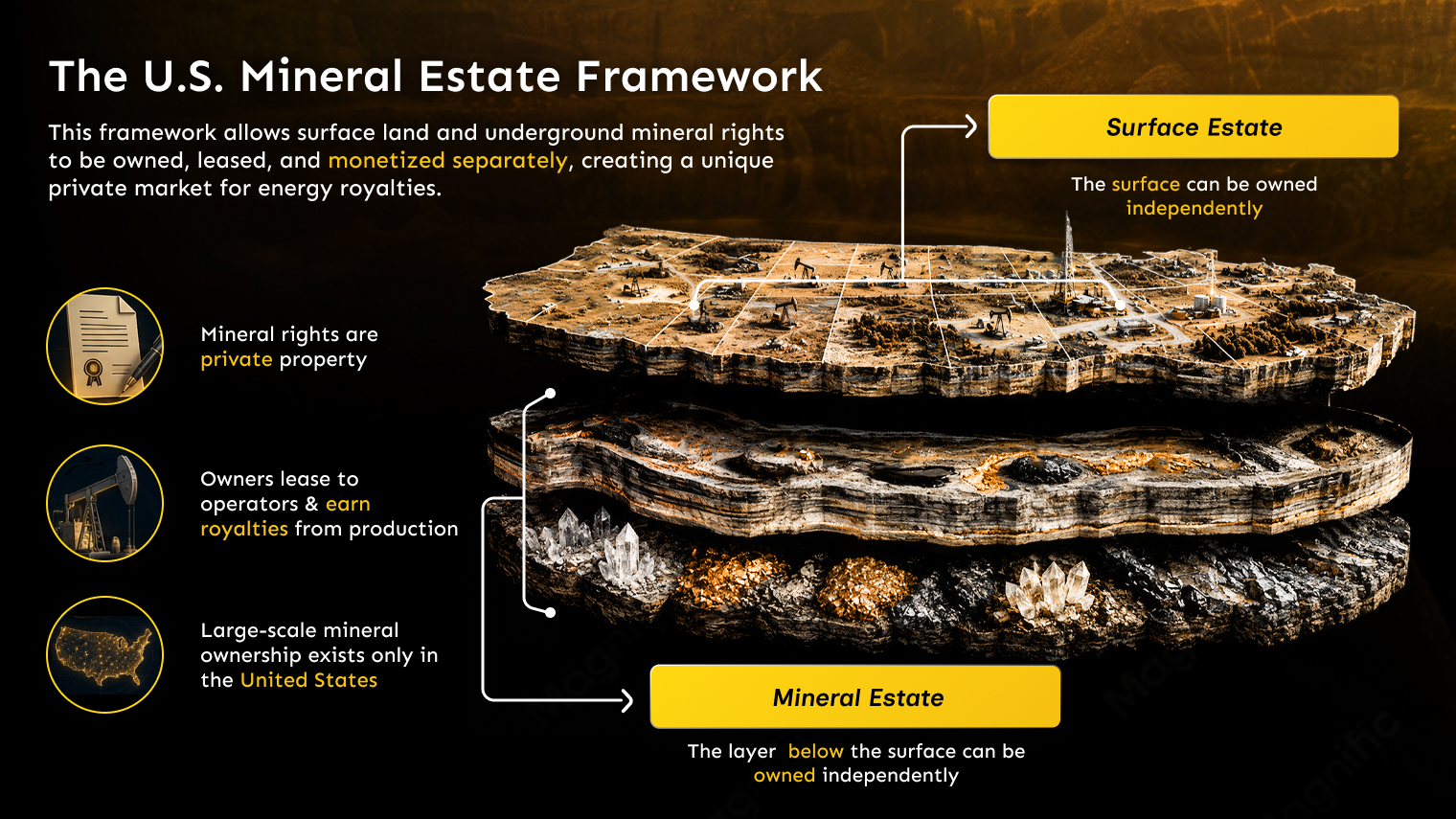

The U.S. exception: a private market in the mineral estate

The United States developed a very different framework. In most producing regions, the mineral estate can be treated as a separate form of real property. That means the rights below the ground can be owned independently from the surface above it. A parcel can therefore have one owner for the surface and another for the minerals. Those mineral rights can be sold, transferred, inherited, and leased in their own right.

That separability is one of the defining features of the asset class. In practical terms, it means mineral owners do not have to drill wells themselves to benefit economically. They can lease their mineral interests to operators, collect an upfront lease bonus in many cases, and then receive an ongoing royalty tied to production if development occurs. In other words, they own the property interest while the operator takes on the capital-intensive work of drilling, completing, and producing the well.

This is also why mineral and royalty interests have long occupied a category of their own:

- They share some traits with real estate, because they are real property interests.

- They share some traits with income assets, because they can generate recurring cash flow.

- They share some traits with commodity-linked derivatives, because revenue rises and falls with production volumes and commodity prices.

…but mineral and royalty interests are not reducible to any one of these buckets.

It is important to keep the nuance intact here. Not every mineral resource in the United States is privately owned. Federal lands, many state-owned lands, tribal lands, and offshore federal resources follow different legal frameworks. The point is not that every American resource is private. The point is that the United States has a deep and scalable private minerals market – especially onshore – that is unusual among major producing nations.

Why this rarity creates both value and friction

Whenever an asset class is both economically attractive and structurally unusual, two things tend to happen at once: the asset becomes valuable, and access becomes messy. That is exactly what happened in mineral interests.

On the value side, private mineral ownership gives investors direct participation in American energy production without requiring them to operate wells. When high-quality mineral interests are leased and producing, owners can receive long-duration royalty income with meaningful inflation linkage because hydrocarbons are sold into real commodity markets. In many structures, the mineral owner also avoids most of the drilling and operating costs borne by the operator.

On the friction side, the market developed in a way that was highly fragmented, paper-heavy, and relationship-driven. Mineral rights have often passed through generations, trusts, estates, family partitions, and thousands of individual transactions. Ownership records can be scattered across county courthouses and title files. Minimum investment sizes have historically been high. Liquidity has been limited. And for investors outside the United States, the barriers have been even higher because the asset class itself is so tied to a uniquely American property system.

This combination is exactly why mineral interests have remained under-owned by the broader global investment market. It is not because the cash flow characteristics are weak. It is because the access path has traditionally been too narrow, too technical, and too operationally burdensome for most investors to navigate.

Why it matters to investors

For investors, the global rarity of private mineral ownership matters because rarity shapes portfolio opportunity. If an asset class exists at scale in only one major jurisdiction, and if access to that asset class has historically been difficult, then the investors who can access it efficiently may be seeing a genuinely differentiated source of return.

Mineral and royalty interests provide exposure to real-world production cash flow rather than to the earnings of an operator or the coupon stream of a bond. They can offer monthly income, inflation-sensitive revenue, long-duration underlying property exposure, and upside from future leasing or drilling activity on the acreage. At the same time, they are not the same thing as direct working interests in wells, where capital calls and operating costs can materially change the risk profile.

That distinction matters even more in a modern portfolio. Many investors already understand stocks, bonds, and listed real estate. Far fewer have access to a real-asset income stream tied directly to U.S. energy production while remaining generally non-cost-bearing at the mineral-owner level. That is part of what makes the asset class so compelling once it can be accessed cleanly.

Why it matters to Mineral Vault

Mineral Vault was built around the idea that a rare, high-quality asset class becomes dramatically more powerful when access frictions are reduced. Mineral Vault I brings together a large, diversified portfolio of U.S. mineral and royalty interests spanning more than 2,500 producing wells, more than 10,000 gross acres, 150-plus operators, and 9 U.S. states. That scale matters because it moves investors away from the concentration risk of a single property or operator and toward a broader stream of American energy cash flow.

Just as importantly, Mineral Vault does not present mineral ownership as a novelty. It presents it as infrastructure for a better investment experience. Through tokenization, a historically fragmented and paper-based market can be transformed into a digital ownership record with clearer provenance, lower administrative friction, easier transferability within the applicable compliance framework, and monthly digital distributions tied to real underlying cash flow.

That bridge from old-world property rights to modern financial rails is what makes the topic so relevant today. The underlying legal foundation is not new. Private mineral ownership in the U.S. has existed for generations. What is new is the ability to package that ownership into a structure that is more transparent, more accessible, and more usable for a broader class of investors, including investors outside the traditional U.S. mineral-rights ecosystem.

Why tokenization is the missing link

Historically, if a global investor wanted exposure to U.S. mineral interests, the practical obstacles were substantial. The investor had to understand title, legal documentation, jurisdictional structuring, operator reporting, cash distribution mechanics, and a market that often moved through specialist networks rather than broad digital marketplaces. Even sophisticated investors frequently chose not to engage, not because the asset class lacked merit, but because the ownership system was too inefficient.

Tokenization changes that equation. Once the underlying mineral interests are properly aggregated and structured, digital ownership records can replace much of the transfer friction that made the asset class so cumbersome. On-chain records can improve provenance after issuance and transfer. Compliance tooling can help preserve lawful access pathways. Reporting can become more standardized and more visible. And cash flow can be distributed in a way that better matches the expectations of modern digital investors.

This is where the rarity of private mineral ownership becomes more than an interesting educational topic. It becomes a strategic advantage. If the United States is one of the only places where this type of asset exists at meaningful scale, and if Mineral Vault can make that asset class more legible and accessible to a global audience, then tokenization is not a cosmetic wrapper. It is the enabling layer that converts a rare property-rights system into an investable digital experience.

A more precise way to think about the opportunity

It is tempting to reduce the story to a simple headline: the U.S. is unique, therefore mineral royalties are valuable. But the better way to think about it is more specific. The rarity matters because it concentrates a distinctive ownership model inside one major market. That ownership model produces a real-asset income stream that most global investors have never had efficient access to. And because access has been so inefficient, the market has historically remained narrower than the underlying economic value would suggest.

Mineral Vault exists to close that gap. By combining professionally managed U.S. mineral and royalty interests with blockchain-native issuance, transparent reporting, and digital distributions, Mineral Vault is not inventing a new asset class. It is opening an old and highly differentiated one to a modern investor base.

Final Thoughts

Private mineral ownership is rare globally because most legal systems reserve subsurface value for the state. The United States developed differently, creating a market where mineral rights can be privately held, leased, and monetized at scale. That difference has made American mineral interests both powerful and hard to reach.

Why does that matter? Because rare ownership structures create rare investment opportunities – but only if investors can actually access them. Mineral Vault is built on the belief that U.S. mineral and royalty interests deserve a broader audience, and that tokenization can finally provide the access layer this asset class has always lacked.

In that sense, the story is larger than mineral rights alone. It is about what happens when a uniquely American property system meets global digital finance. And that is exactly where the next chapter of this asset class begins.

Why Mineral Interests Are One of the Most Misunderstood Asset Classes in America

Why Mineral Interests Are One of the Most Misunderstood Asset Classes in America  What Actually Determines a Royalty Distribution Month to Month?

What Actually Determines a Royalty Distribution Month to Month?  Why Tokenize Mineral Interests?

Why Tokenize Mineral Interests?